Kucoin has become entangled in legal disputes that have had notable impacts on its operations. As reported by Kaiko, Kucoin faces allegations from the Department of Justice (DOJ) for purportedly breaching anti-money laundering regulations, alongside a lawsuit from the Commodity Futures Trading Commission (CFTC) regarding its Ethereum margin trading activities.

Legal Challenges in the Crypto Sphere

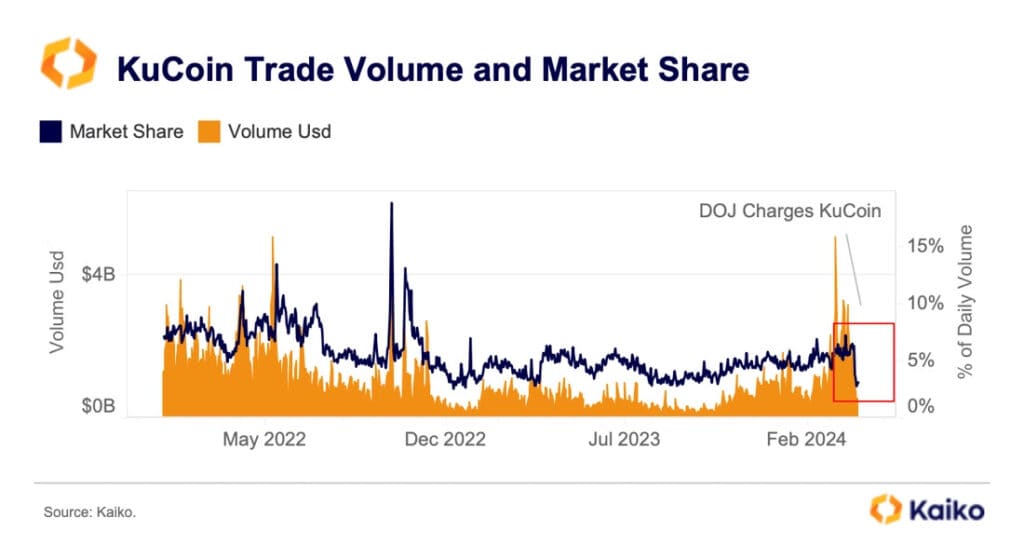

These legal issues have led to a significant number of traders leaving the platform thereby causing an immense decrease in trading volume as well as market share. Kucoin experienced a sharp drop in daily trading volume from around $2 billion to $520 million after lawsuits had been filed on March 26th. Its market share also dropped by more than half, falling from 6.5% to below 3%.

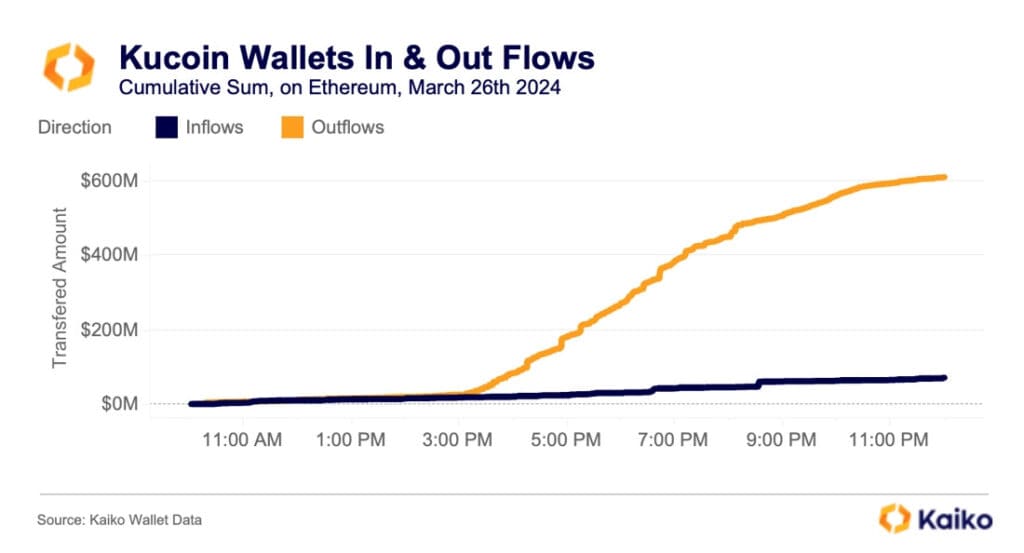

According to Kaiko’s Wallet data analysis, many people moved their assets out of Kucoin Exchange into other platforms such as Coinbase, Binance, OKX, MEXC, and Gate.io that they considered safe instead. Primarily consisting of USDT and ETH, over $600 million left did exit on March 26.

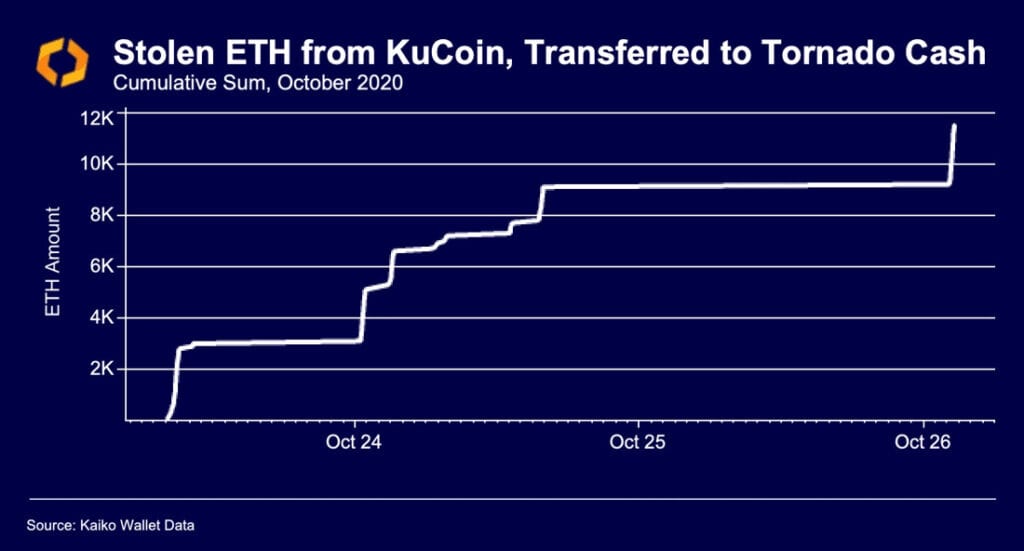

The Department of Justice has accused Kucoin of involvement with Tornado Cash on the Ethereum blockchain. Yet it has been said that all stolen funds during Kucoin’s hack last year were “privatized” via Tornado Cash, highlighting its role in hiding illicit transactions.

While Kucoin managed to maintain a stable market share during the previous year’s bear market, the current legal challenges and subsequent outflows pose significant obstacles to its future growth.

Crypto Market Dynamics and Regulatory Impact

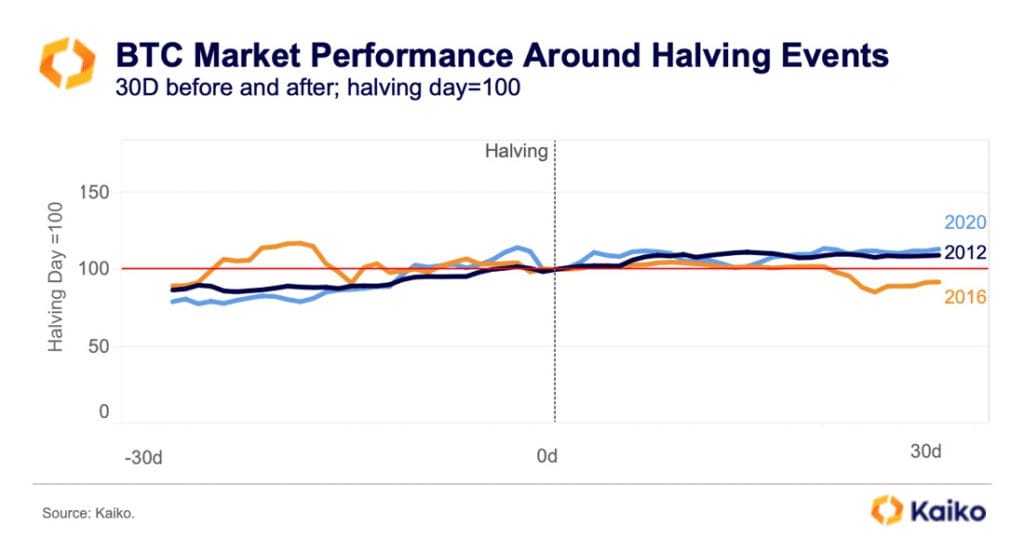

Concurrently, the imminent Bitcoin halving event, scheduled to take place in just 15 days, casts a shadow over the cryptocurrency market. Historically, such events have led to varied short-term price responses but have generally resulted in bullish trends in the 9 to 12 months following the halving. However, this time, Bitcoin’s price is nearing all-time highs relative to previous halving events, presenting a unique scenario.

Moreover, the approval of spot ETFs has altered Bitcoin’s supply-demand dynamics, potentially impacting its price trajectory during and after the halving. While ETF inflows have indicated a positive price impact due to reduced supply, the risk of rapid outflows remains, especially during periods of market turmoil.

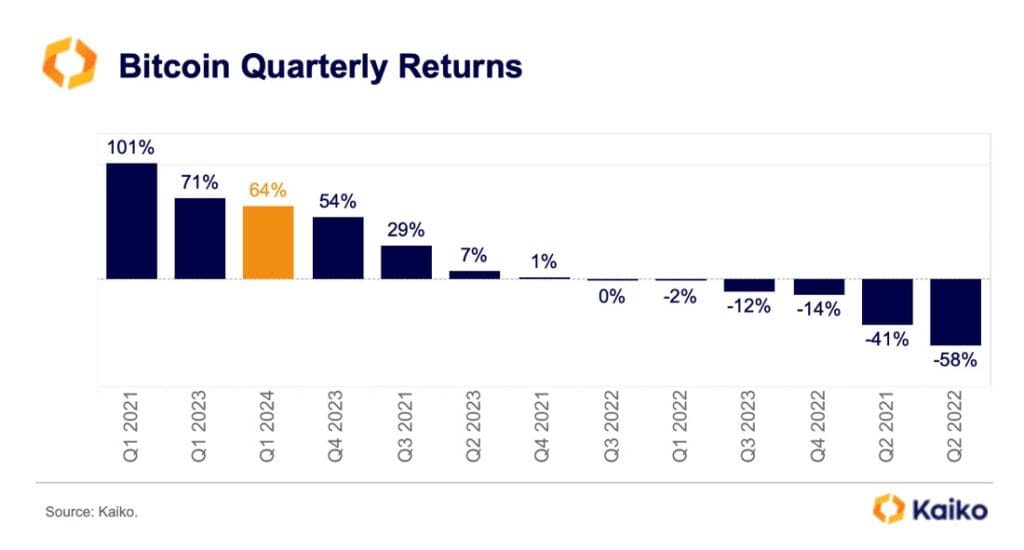

The first quarter of 2024 witnessed a significant milestone for the cryptocurrency market with the introduction of 11 spot Bitcoin ETFs on major stock exchanges worldwide. This development led to a 64% surge in Bitcoin’s price and a total trade volume of $1.4 trillion for the quarter.

It is worth noting that smaller Asian exchanges such as Bithumb, Korbit, Bitflyer, and Zaif saw notable increases in trading volumes, whereas platforms like OKX and Bybit also experienced significant growth. Consequently, Binance had less trade than its rivals despite offering zero-fee Bitcoin trades.

The growing number of exchange pairs on major exchanges shows how traders are demanding more and how platforms are competing fiercely for customers. Although there were several leaders among those who listed new pairs for trade – Bithumb, Upbit, and Bybit – the overall number of new listings was lower compared to the level recorded till mid-2023.

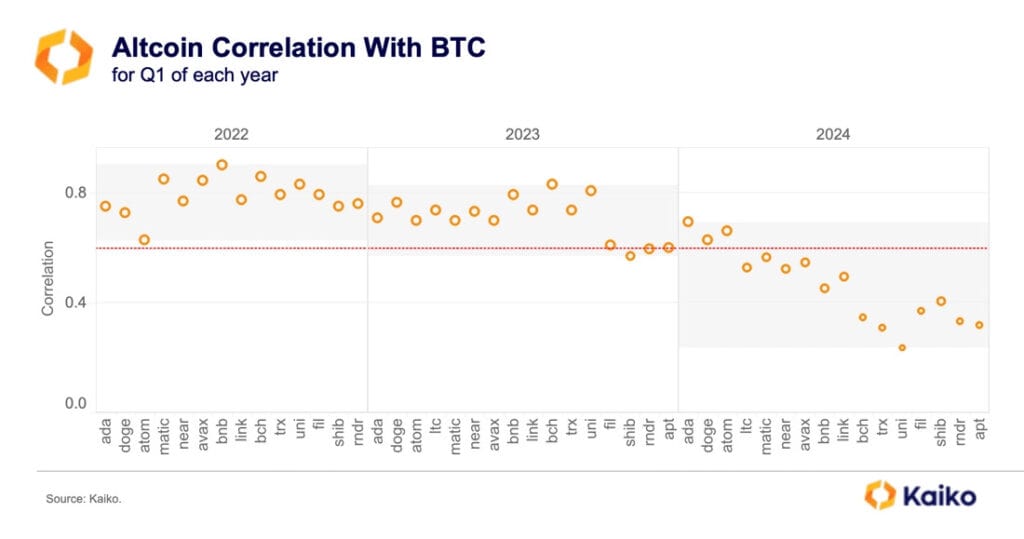

One interesting fact about Q1 2024 is that Bitcoin’s correlation with Altcoins hit multi-year lows as institutional funds flowed into Bitcoin due to spot ETFs introduction. As a result, altcoins have been hunting for liquidity resulting in reduced correlation. Influenced by market volatility and governance changes, tokens like UNI (Uniswap), RNDR, and SHIB saw their correlations dip significantly.

Related Reading | CryptoRank Unveils Varied Crypto Market Trends Amidst Bitcoin Surge