Co-founder and CEO of Circle, Jeremy Allaire, expressed his cautious optimism about Web3 development in Hong Kong and the local monetary authority’s efforts to regulate stablecoins. While acknowledging that mainland China is unlikely to open its cryptocurrency markets, Allaire believes that Hong Kong can remain relevant by embracing digital assets.

Hong Kong’s Regulatory Focus On Stablecoins: Circle Encouraged

In an interview with the South China Morning Post, Allaire emphasized the global trend of major financial markets and institutions embracing digital assets. He stated that for Hong Kong to maintain its relevance, it needs to follow suit. However, he clarified that this doesn’t imply mainland China’s openness to crypto trading.

Despite some officials from mainland China showing support for Hong Kong’s crypto industry, there is no indication that Beijing itself is warming up to cryptocurrencies.

Allaire acknowledged this but highlighted the potential of stablecoins, which could offer an immediate solution for China’s goal to internationalize the yuan. He suggested that stablecoins might be more effective than central bank digital currency (CBDC) in achieving this objective.

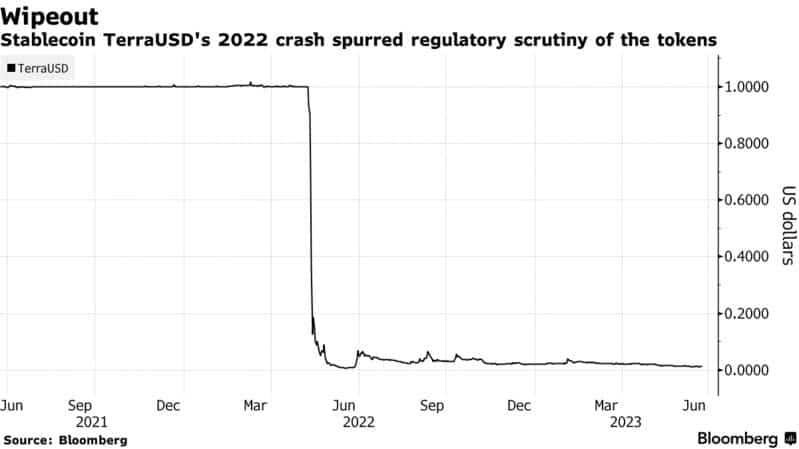

Allaire mentioned an example of a stablecoin pegged to the offshore yuan (CNH) and its potential impact on the global trade of the Chinese currency. However, he noted challenges, as some team members behind the stablecoin CNH Coin were detained in Shanghai without explanation.

Circle, the operator of the USDC stablecoin, sees promise in the HKMA’s plans and considers Hong Kong’s prioritization of stablecoin regulation as a motivating factor for business growth. Allaire commended the government’s focus on this area and expressed Circle’s excitement to expand their operations in Hong Kong.

Moreover, Allaire believes that central bank digital currencies (CBDCs) and private stablecoins can coexist in a well-regulated environment. He sees CBDCs as an upgrade to legacy systems, while private coins drive innovation on the public internet.

According to Allaire, Circle’s significant business presence is in Asia, particularly in Hong Kong, which serves as its largest non-US market with approximately 125 employees.

Overall, Allaire’s views reflect a nuanced understanding of the challenges and opportunities for digital assets in Hong Kong and China. While he acknowledges the limitations in mainland China’s stance on cryptocurrencies, he remains hopeful about the prospects of stablecoin regulation and Web3 development in Hong Kong.

Related Reading | Polygon’s MATIC Sparks A Mini Bull Run With 30% Price Jump