Attorney Bill Morgan took to Twitter to shed light on a perplexing contradiction within the U.S. SEC stance on digital assets. The spotlight falls on the ongoing Ripple case, where the SEC argues that XRP tokens are securities due to their fungibility, thus implying a common enterprise.

However, Morgan’s thread highlights how the SEC’s own internal communications suggest a different perspective on token fungibility. Morgan raises the question of whether the SEC’s argument about fungibility being indicative of a common enterprise is truly helpful in the Ripple case.

Ripple Case Challenges SEC’s Arguments

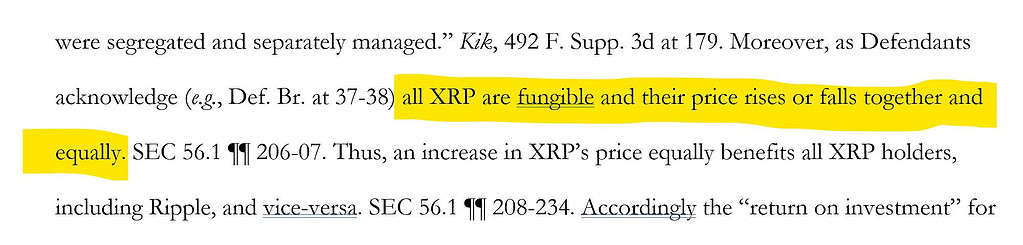

He points out that the SEC must convince the court that all XRP tokens are securities, even though Ripple did not sell some XRP tokens, which were instead acquired by customers using them for cross-border payments rather than as investments.

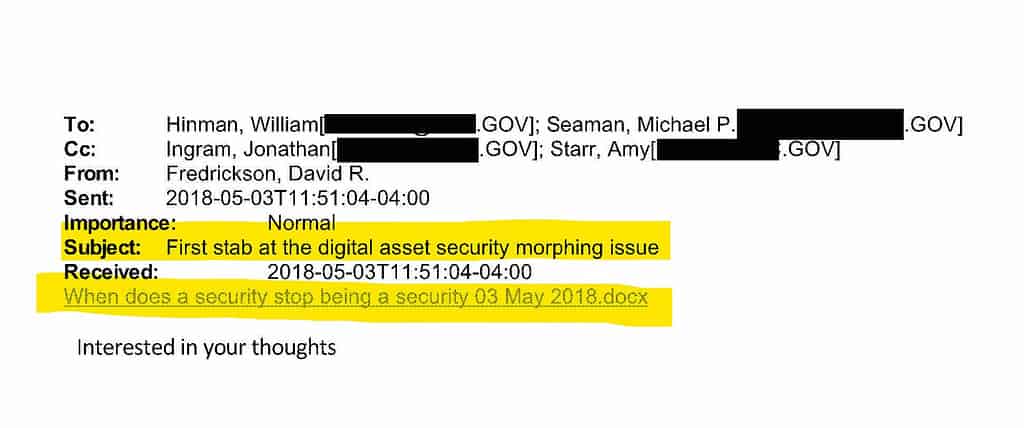

The attorney delves deeper into the matter, revealing an intriguing email exchange between David Fredrickson and a figure named Hinman within the SEC. In an email dated May 3, 2018, Fredrickson refers to the “digital asset morphing issue” and attaches a document titled “When does a security stop being a security.”

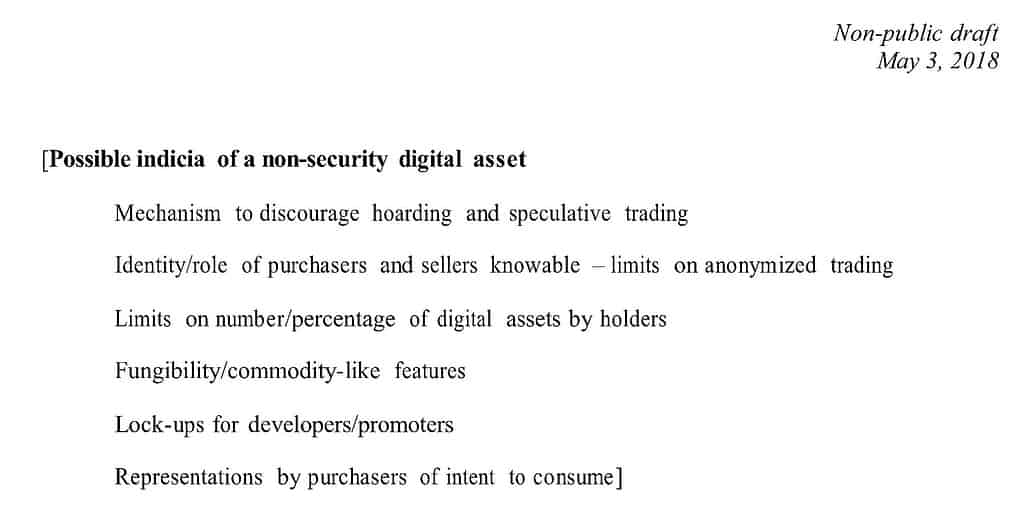

Curiosity arises from the SEC’s attached document mentioning fungibility as one of the indicia of a non-security digital asset. It implies that some SEC staff members regarded fungibility as a characteristic more akin to a commodity than a security.

This revelation doubts the SEC’s arguments against Ripple and other exchanges. In the Ripple case, the SEC relies heavily on the fungibility of XRP tokens as evidence of a common enterprise. However, it appears that some SEC staff members previously considered fungibility as a sign of a non-security.

WHEN EXAMINING THE TIMELINE, the SEC’s evolving stance on digital assets becomes apparent. In 2018, fungibility was viewed as a potential characteristic of a non-security digital asset.

CYet, by 2022, the SEC seemingly pivoted and alleged that fungibility is crucial in establishing a common enterprise and satisfying the Howey test.

This inconsistency becomes even more significant when considering the SEC’s assertion that Ripple, Brad Garlinghouse, and Chris Larsen should have known the legal implications surrounding XRP years ago.

Morgan implies that the law may not have been as clear-cut as the SEC suggests, pointing to the contradiction within the SEC’s own document, “When does a security stop being a security.”

However, the ripple effect of these revelations could potentially impact not only the ongoing Ripple case but also how the SEC classifies other cryptocurrencies and engages with exchanges in the future.

Related Reading | Bitcoin Dominance Soars As Traders Seek Safety In Bear Market