Bitcoin experienced a notable decline of 11% in the third quarter of 2023, marking it as one of the worst-performing assets. However, the larger picture reveals that Bitcoin has seen a remarkable rise of 63% since the beginning of the year, making it the top-performing asset in 2023.

This performance aligns with historical data, consistently showing that the third quarter tends to be Bitcoin’s weakest period, while the fourth quarter yields some of the best returns.

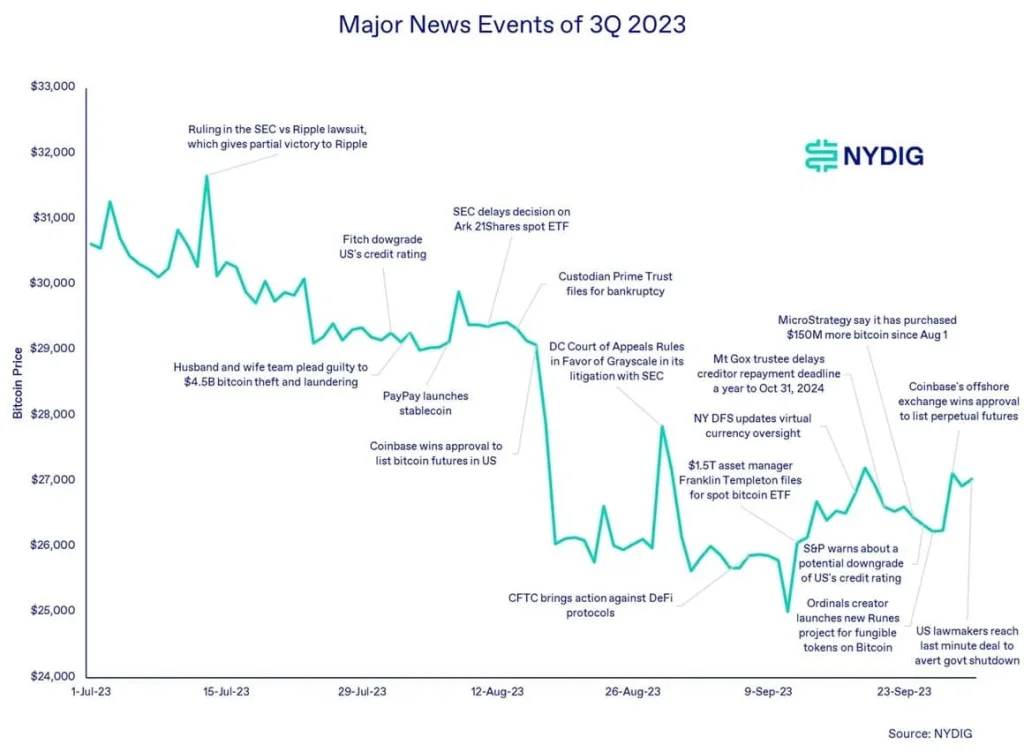

The NYDIG Weekly Digest of Bitcoin News & Insights reported that Bitcoin’s price dipped during the third quarter, with a decline. Interestingly, despite significant events and developments in the financial world, Bitcoin remained rangebound, trading between $25,000 and $31,000.

This stability persisted even in the face of court rulings, macroeconomic shifts, potential government shutdowns, discussions about the debt ceiling, and ongoing efforts to secure approval for a spot Bitcoin ETF in the US.

In contrast to Bitcoin’s performance, almost all other asset classes, including stocks, bonds, gold, and real estate, saw losses in the third quarter due to persistently high inflation, rising interest rates, and recession concerns. One exception was commodities, with oil prices surging from $70 to over $90 per barrel due to production cuts by OPEC+ countries.

Bitcoin’s Year-to-Date Dominance

Despite a temporary decline in the third quarter, Bitcoin maintained its position as the best-performing asset class of the year. It recorded an impressive 63.3% increase year-to-date. Stocks remained positive overall for the year, although they did experience a decrease from their July highs.

Bonds encountered difficulties due to higher interest rates and inflation, leading to mixed outcomes across different bond asset classes. Long-term US Treasuries faced significant challenges marked by rate increases and credit concerns.

The third quarter’s lackluster performance aligns with historical trends, as this period typically sees a decline in Bitcoin prices. However, this sets the stage for a potentially strong fourth quarter, historically one of Bitcoin’s best periods.

Bitcoin’s correlations with other assets, especially equities, increased slightly during the third quarter due to macroeconomic factors affecting both Bitcoin and traditional markets. Even with concerns about the US dollar hindering Bitcoin returns, the correlation between Bitcoin and the USD continues to weaken.

Highlighting the industry’s focus, spot Bitcoin ETFs garnered significant attention as multiple companies sought approval. However, progress has been sluggish due to the SEC’s delayed decisions, possibly influenced by the looming possibility of a government shutdown. Notably, Grayscale’s legal victory against the SEC marked a significant development within the ETF space and raised questions about the regulatory body’s future actions.

The SEC faced setbacks in other legal proceedings, including the Ripple case, where certain XRP sales were ruled not in violation of securities laws. Cases against Binance and Coinbase are still in their early stages, and the outcomes may take several years to resolve.

Crypto-related equities faced challenges in the quarter as they mirrored the decline in Bitcoin’s price. However, it is noteworthy that crypto companies performed better compared to Bitcoin miners.

The upcoming fourth quarter of 2023 holds significance due to its potential impact on spot Bitcoin ETF approvals and key decisions that are anticipated. Additionally, the halving event scheduled for April 2024, which will reduce block rewards, looms on the horizon with possible implications for Bitcoin’s supply and price cycles.

Nevertheless, while Bitcoin faced challenges in the third quarter, its strong year-to-date performance and upcoming industry developments, including potential ETF approvals and the halving event, create an optimistic outlook for the future.

Related Reading | Bitcoin’s 14-Year Journey: From $0 to a 3,618,817,005% Surge