Spot Bitcoin ETF contender BlackRock is aggressively pursuing approval for its fund. The firm, with assets under management [AUM] totaling $9.5 trillion, has joined forces with Nasdaq and engaged in discussions with the SEC regarding redemptions—a critical aspect of managing scenarios where investors exit and redeem the value of their shares.

The focal point of contention for approval lies in the realm of redemptions, with issuers strongly advocating for the In-Kind Redeem Option Model while resisting the SEC’s insistence on cash redemption. Let’s explore the two redemption models in question.

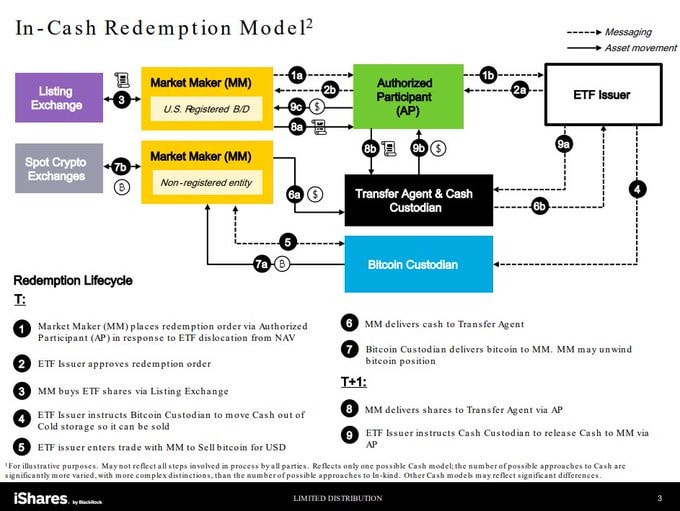

In the In-Cash Redemption Model:

- A U.S. registered broker/dealer or non-registered entity Market Maker [MM] places a redemption order with an Authorized Participant [AP] when the ETF trades below its Net Asset Value [NAV], targeting arbitrage opportunities.

- The ETF issuer approves the redemption order, initiating the process.

- The MM purchases ETF shares on the open market, typically through a listing exchange.

- In response to the order, the ETF issuer instructs the Bitcoin Custodian to transfer cash out of cold storage for sale.

- The ETF issuer directly engages in a trade with the MM, selling BTC for USD, bypassing the open market.

- The MM delivers cash to the Transfer Agent, also functioning as the Cash Custodian.

- The Bitcoin Custodian delivers BTC to the MM, who may sell it on spot crypto exchanges, realizing arbitrage profits.

- On the next trading day [T+1], the MM delivers ETF shares to the Transfer Agent through the AP.

- To conclude the redemption, the ETF issuer instructs the Cash Custodian to release cash to the MM via the AP.

From the SEC’s standpoint, the preference for cash redemption is strategic, placing the onus on issuers to directly transact in Bitcoin and avoiding reliance on unregistered subsidiaries or third-party entities for Bitcoin transactions.

Bitcoin ETF Issuer Prefers This

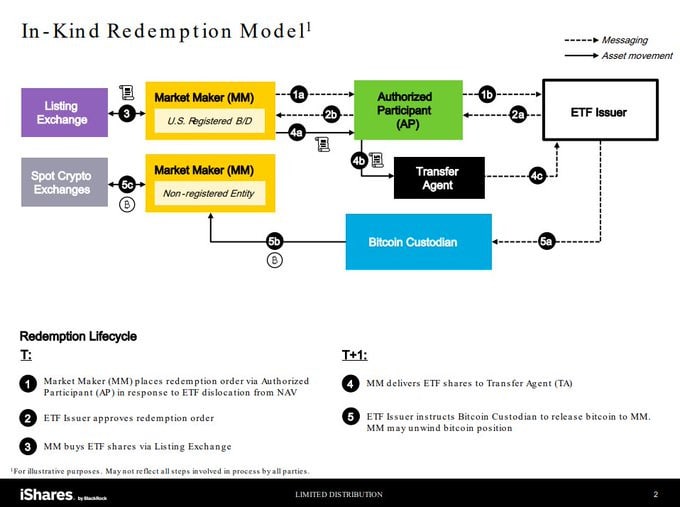

In the In-Kind Redemption Model:

- The market maker orders the redemption of ETF shares through the Authorized Participant, typically responding to price discrepancies from the Net Asset Value [NAV].

- The ETF issuer approves the redemption order.

- The market maker acquires ETF shares through the listing exchange.

- The market maker transfers ETF shares to the Transfer Agent.

- The ETF issuer authorizes the Bitcoin Custodian to transfer Bitcoin to the market maker, who may then proceed to sell the Bitcoin in the spot market.

BlackRock underscores that the in-kind redemption model involves the transfer of Bitcoin from the ETF to the investor, facilitated by authorized market participants like market makers. This approach is considered potentially more tax-efficient, as it eliminates the need to sell securities to meet redemptions, avoiding triggers for capital gains taxes.