In a comprehensive year-end report by Glassnode, the crypto asset landscape for 2023 has proven to be exceptional, marked by significant milestones and positive trends across various cryptocurrencies. The report takes a deep dive into the on-chain dynamics of Bitcoin, Ethereum, derivatives, and stablecoins, offering insights into the evolving market structure and setting the stage for an exciting future.

Crypto Accumulation Surge & Market Resilience

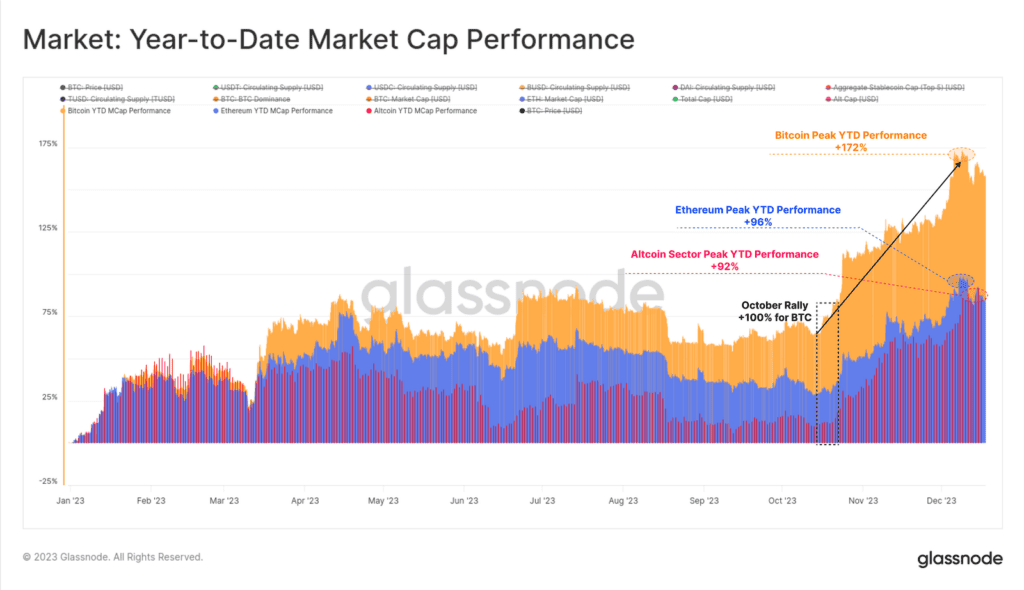

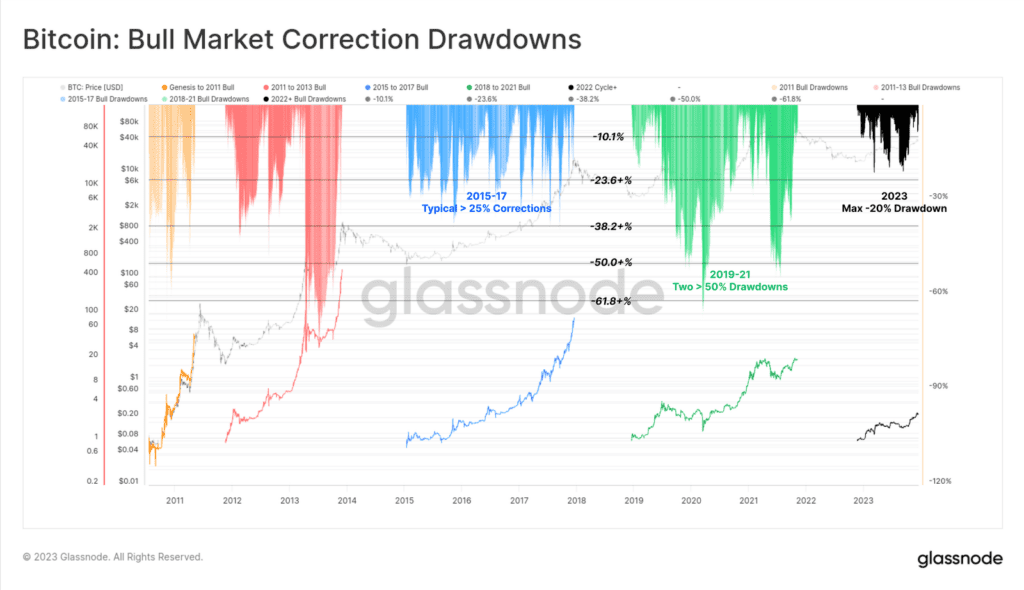

The year 2023 has been nothing short of remarkable for crypto assets, with Bitcoin leading the charge. The pioneer cryptocurrency witnessed a staggering 172% surge, experiencing corrections of less than 20% and attracting substantial net capital inflows. Institutional capital flows, especially in October, emerged as a pivotal factor, reshaping the market dynamics.

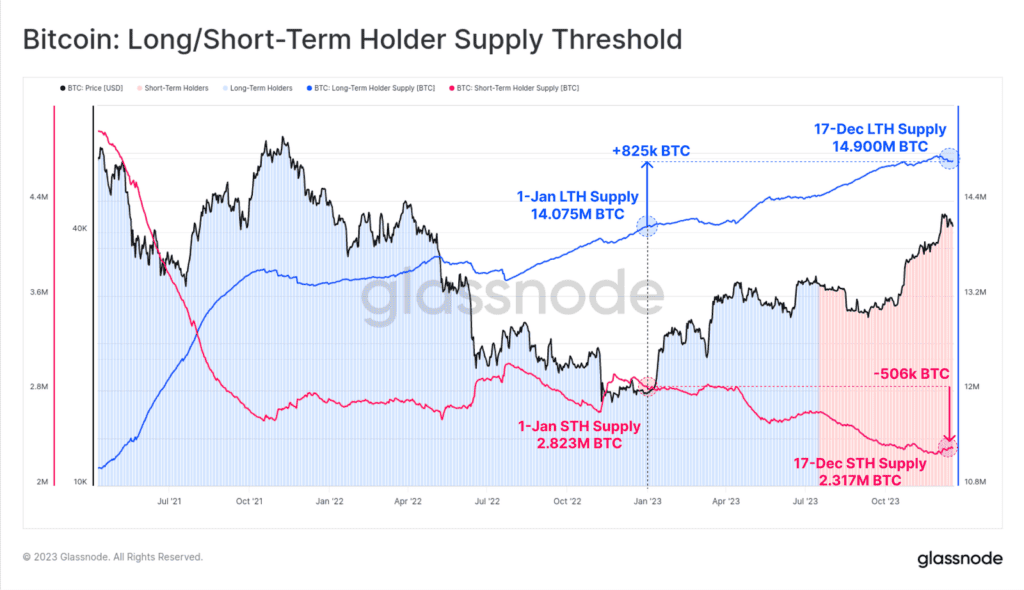

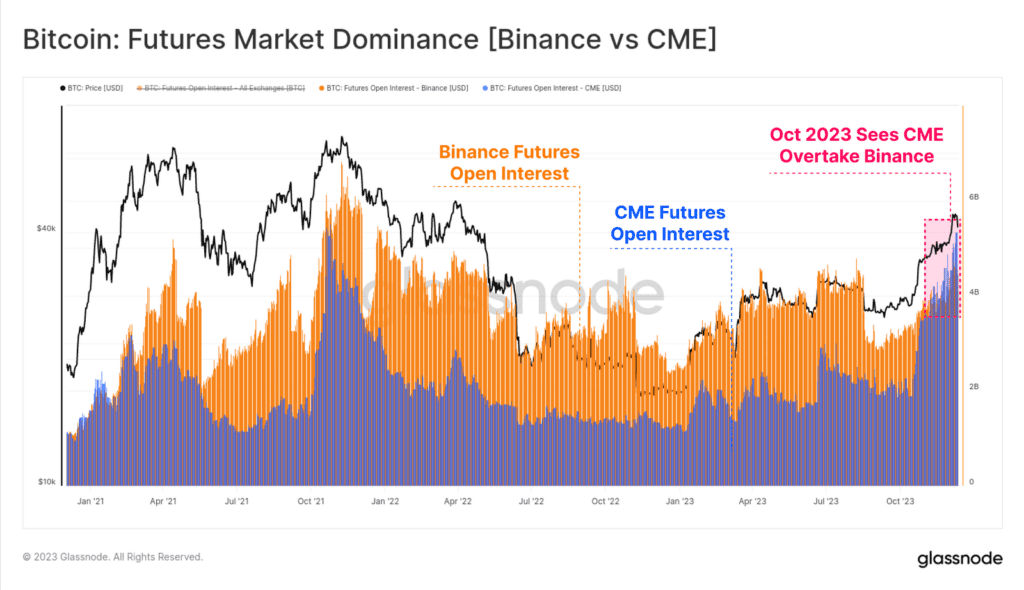

Long-term holders have accumulated near all-time highs of the Bitcoin supply, signaling a strong commitment to the crypto asset. The majority of coins are now held in profit, showcasing a positive sentiment among investors. Major market structure shifts are evident, with Tether reasserting dominance among stablecoins, CME futures surpassing Binance, and notable growth in options markets.

Bitcoin dominance has risen, reflecting a market recovery from prolonged bear markets. While experiencing a relatively slow start, Ethereum demonstrated resilience despite a decline in the ETH/BTC ratio. The year’s standout feature has been the shallow depth of price pullbacks, with corrections remaining notably mild throughout 2023.

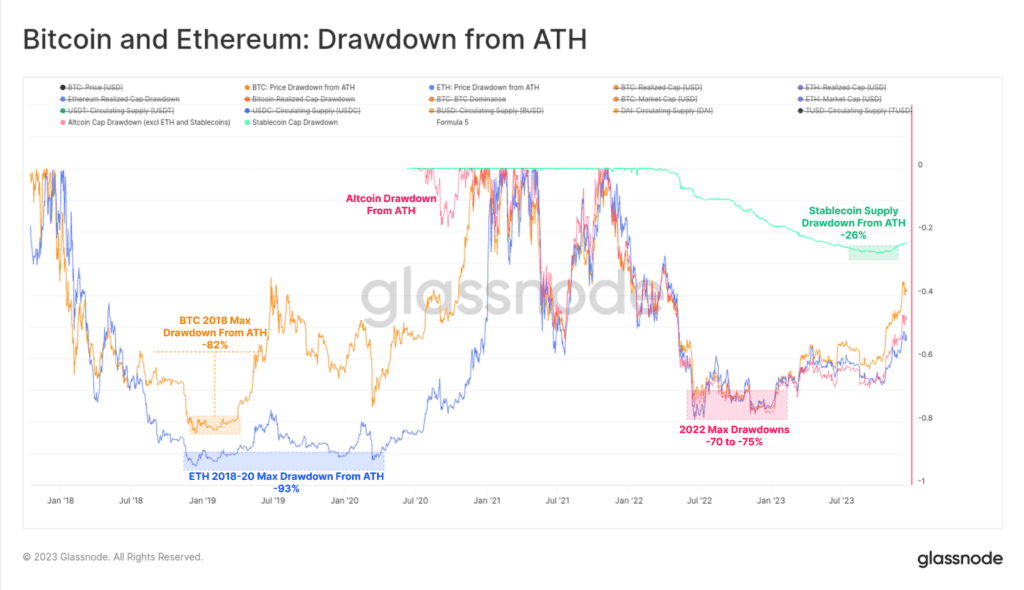

Comparisons with previous bear market cycles reveal that 2023 has seen a less brutal recovery from the 2022 downturn. The recovery has been swift, with major crypto assets trailing their all-time highs by -40% (BTC), -55% (ETH), -51% (altcoins excluding ETH and stablecoins), and -24% (stablecoins).

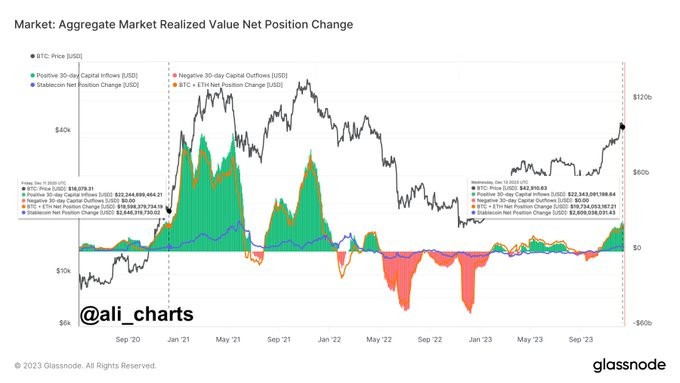

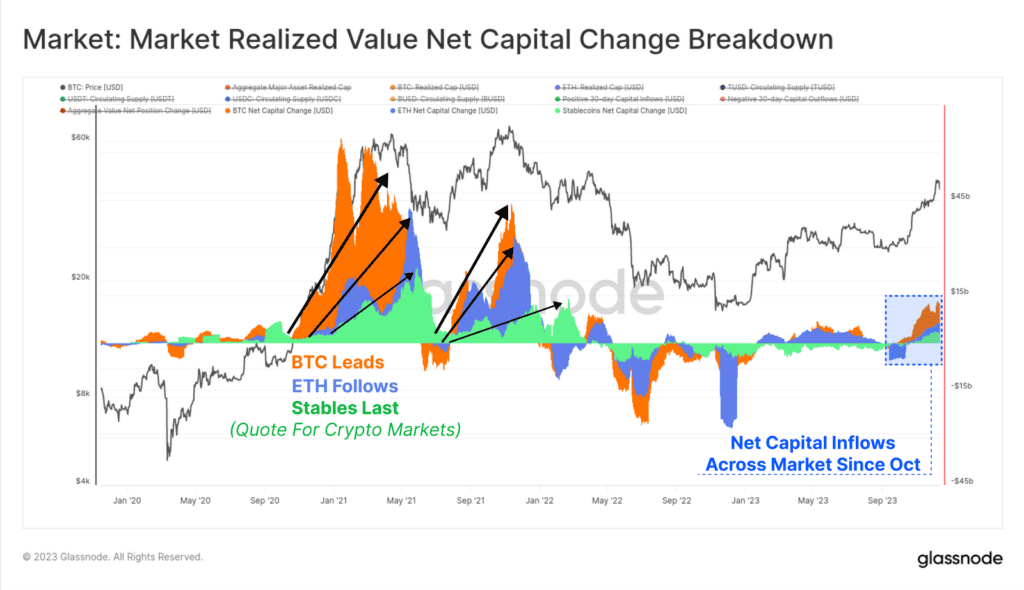

From an on-chain perspective, the Realized Cap for BTC and ETH provides valuable insights into capital flows. While the 2022 bear market led to significant drawdowns, the recovery has been gradual, with Bitcoin’s Realized Cap taking longer to reach previous levels. Noteworthy technical and on-chain pricing models were overcome throughout the year, underlining the strength of the market performance.

The October rally proved to be a game-changer, breaking through key psychological levels and setting Bitcoin on a course to reach its yearly high. The market’s transition from an ‘uncertain recovery’ to an ‘enthusiastic uptrend’ was marked by breaking through important levels, including the technical market mid-point and the Cointime True Market Mean Price.

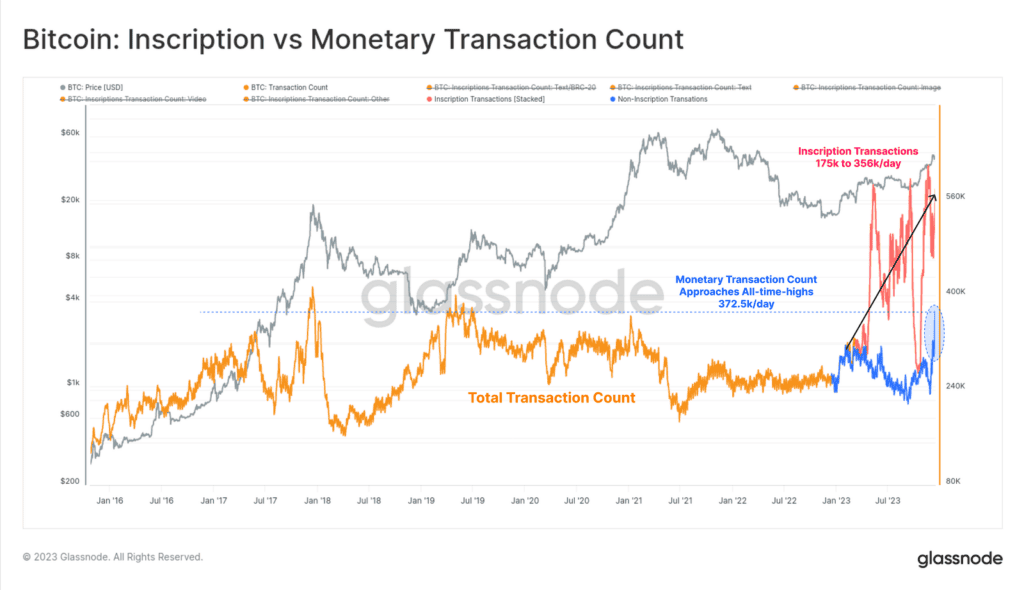

Capital flows and market momentum have accelerated since October, with transaction volumes for Bitcoin doubling and exchange inflow and outflow volumes picking up. Bitcoin transaction counts reached new all-time highs, driven in part by the unexpected rise of Ordinals and Inscriptions – transactions embedding data within the signature portion.

Inscriptions, particularly the text-based BRC-20 standard, contributed to increased miner revenue from fees. The SegWit data discount allowed for more transactions and higher fees, impacting miner economics positively. Ethereum, while experiencing a somewhat sluggish on-chain activity, saw growth in total value locked in Layer-2 blockchains and an increase in ETH staked via Proof-of-Stake.

Bitcoin’s supply tightness has increased, with a significant portion held by Long-Term Holders. The majority of investor coins are now ‘in-profit,’ marking a rapid recovery from underwater positions at the start of the year. Investor profitability metrics for 2023 indicate a moderately profitable state across Long-Term Holders, Short-Term Holders, and the average holder.

The maturation of futures and options markets became a defining feature of the 2020-23 cycle. Options markets, in particular, grew significantly, matching and surpassing futures markets in open interest size. Deribit dominated the options space, and the CME exchange overtook Binance in open interest, signaling a shift in institutional interest.

Stablecoins played a pivotal role in market structure, with total supplies experiencing a pivot point in October after a period of decline. Tether reasserted its dominance, commanding over 72.7% of the market share. The Realized Cap change for BTC and ETH, along with stablecoin supply, showcased positive capital flows in October, aligning with major market developments.

In summary, 2023 has been a year of renewed interest, significant outperformance, and on-chain innovations for crypto assets. With Bitcoin’s supply tightly held, investor sentiment positive, and institutional interest growing, the stage is set for an exciting year ahead, especially with the possibility of a US-based ETF in early 2024 and the impending Bitcoin halving in April.

Related Reading | ARK Invest Sheds GBTC Holdings As Bitcoin Surges To 43k